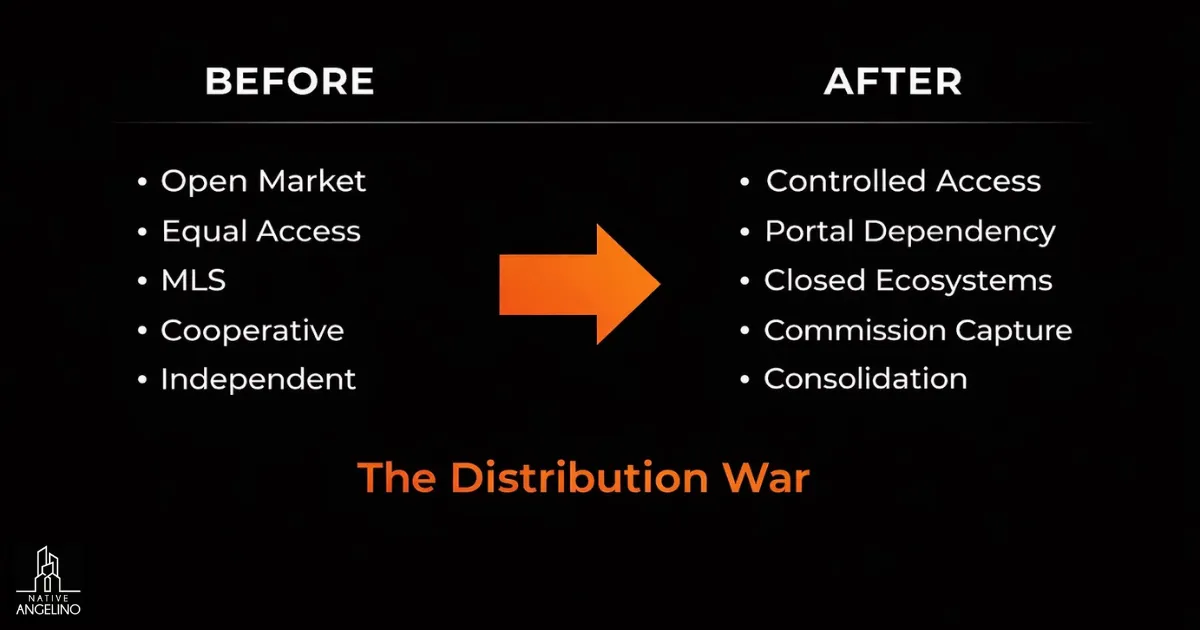

The Distribution War

The central battle is no longer over market share. It is over who controls the first point of listing exposure and consumer attention.

Control of Listing Flow Matters More Than Traditional Market Share

Traditional market share is measured in closed transactions. The new competition is measured earlier, at the moment a listing originates and first reaches a consumer.

The firm that controls where a listing first appears controls which buyers see it, which agents represent those buyers, and whether the transaction stays inside the firm’s ecosystem.

This is the distribution war. It is a sequential set of business decisions made by every major player over the past eighteen months, each designed to move competitive advantage from transaction to pretransaction.

How Redfin Zillow and Brokerage Alliances Reshape Access to Inventory

The Compass and Redfin agreement routes Coming Soon and Private Exclusive listings to Redfin before MLS entry, without displaying days on market or price reduction history. Zillow Preview routes premarket listings from partner brokerages to Zillow and Trulia before MLS activation, with financial incentives to listing agents whose buyers close through a Zillow Preferred Agent. eXp partnered separately with Realtor.com and Homes.com.

Each program is positioned as pro consumer. Each one routes leads back to the originating brokerage or portal partner.

I covered this dynamic in Compass vs Zillow Is Compass Just Redfin on Steroids Part 1 and Compass vs Zillow Dirty Little Secret Part 2 in July 2025. The argument that Compass’s listing strategy was primarily an economic play rather than a consumer service was not the popular view when I first published the podcast Is Compass Just Redfin on Steroids in November 2023.

It is residential brokerage consensus now.

The Weakening of the MLS

The MLS was built on cooperative access. A listing enters a shared database. Every participating agent and every consumer sees the same information at the same time.

Sellers benefit from the broadest possible pool of buyers. These shifts threaten to reduce the MLS from central marketplace to a secondary node in a broker controlled network.

How Premarketing and Preview Systems Bypass the Cooperative Model

Coming soon programs, Zillow Preview, and private listing networks all route listings through proprietary channels before or instead of that cooperative system. Some comply technically with local MLS timing rules.

None serve the cooperative principle the MLS was built to protect.

The distinction between technical compliance and actual intent is exactly where consumers get misled.

Clear Cooperation Compliance Claims and the Fight Over MLS Authority

NAR’s Clear Cooperation Policy required listings to reach the MLS within one business day of public marketing. In March 2025, NAR amended the rule to let local MLSs set their own premarketing windows.

Compass, Rocket, and Redfin then sent that open letter calling out local MLSs including CRMLS for what they described as unwillingness to change.

NAR responded by defending the cooperative marketplace’s pro consumer benefits without addressing the structural incentive problem the letter raised. That nonanswer is its own answer.

The fight over Clear Cooperation is a fight over whether the MLS retains authority to define when and where listings must appear. Compass’s position is that it does not.

Why the MLS Risks Becoming One Node in a Broker Controlled Network

If the largest portals and brokerages build premarket channels that offer agents better leads, more financial incentives, and stronger recruiting tools than the cooperative MLS system, agents will use those channels.

Over time, the MLS becomes secondary distribution, not primary. That changes what a consumer sees when they search for homes, and it changes it in favor of large affiliated firms over independent buyers and sellers.

Industry analyst Rob Hahn put it plainly after the Zillow Preview launch: “They’re absolutely screwed.” That is not hyperbole. It is a structural observation.

The Anti Consumer Reality

When a listing agent is rewarded for keeping a transaction inside the firm’s ecosystem, the advice that agent gives the seller is structurally compromised. That is not a character judgment.

It is how incentives work.

Reduced Exposure Hidden Information and the Risk of Steering

A seller who lists as a Private Exclusive before reaching the open market is, by definition, selling to a smaller pool of buyers than the market contains.

Compass’s own data claims premarketed listings achieve a 2.9 percent higher average close price. Zillow’s own research finds the opposite.

These findings are not reconcilable. They reflect different methodologies, different market conditions, and different incentives in how the data gets presented.

What is not in dispute is this: the seller’s interest in maximum exposure and the agent’s interest in internal commission capture are in direct conflict inside the same transaction.

I covered this in Zillow Got You Started I Closed the Deal and Real Estate Fees Are Broken Disruption and Frustration in May 2025. The incentive structure was visible then. It is more visible now.

Why Internal Matching and Double Sided Incentives Raise Fairness Concerns

When a listing agent at a large brokerage routes a buyer from inside the same firm to a private exclusive listing, the brokerage earns both sides of the commission. That financial incentive is real, measurable, and in direct tension with the obligation to expose the seller’s property to the broadest market.

I asked this question directly in the May 2025 short Real Estate Brokerages Pyramid Scheme or Business Model. The structural critique stands.

A compensation model that rewards internal routing over open market exposure has an anti consumer bias built into its design.

The Oligopoly Reality

Oligopolistic competition means a small number of dominant firms control enough of the market structure to shape how the entire market functions. That is not a future risk in residential real estate.

It is the current condition.

Less Innovation and More Oligopolistic Competition

Compass International Holdings accounts for the mid 20s of total transaction volume. Zillow controls the majority of consumer portal traffic.

The alliance forming between these entities and their brokerage partners is not a competitive response to consumer demand. It is a structural consolidation of market power presented in the language of innovation.

I have watched this play out in financial services and media. The incumbents consolidate before compression reaches full force.

The consolidation provides temporary margin protection. Consumers and smaller market participants absorb the cost.

Where this concentration leads is a question the current data is already beginning to answer. That answer deserves its own analysis.

I covered the early case for this in Compass to Buy Anywhere Real Estate.

The Long Term Risks for Pricing Power Access and Market Transparency

Concentrated control reduces the competitive pressure that disciplines pricing. Reduced price competition means consumers pay more than they would in a genuinely competitive market.

Portal dominance means consumers see a curated version of inventory rather than a complete one. Brokerage dominance means the advice consumers receive is shaped by the advisor’s platform affiliation rather than the client’s actual interest.

None of these outcomes are inevitable. All of them are structurally incentivized by the market architecture currently being built.

Whoever controls first exposure controls the lead. Whoever controls the lead controls the commission.

Our Platforms

P.O. Box 18044

Beverly Hills CA 90209